Are you retired but not yet age 65? If so, you may be surprised to learn that pulling just a little extra from your portfolio this year could trigger the loss of thousands of dollars in health insurance subsidies.

At Curio Wealth, we’re actively helping clients avoid outcomes like this, which stem from an important change to the Affordable Care Act (ACA) taking effect in 2026.

It’s crucial for you to know about this change so you can navigate it successfully, too—we’ll share some of the tactics we’re using in this blog.

Want more hands-on help protecting your retirement nest egg? Let’s talk!

What is the 2026 ACA change?

Here’s the backstory:

When the Affordable Care Act was passed in 2010, it was the beginning of the Health Insurance Marketplace, a place where people of any income level could shop for private, ACA-approved health insurance plans.

Subsidies were available for enrollees who needed financial assistance; these were called premium tax credits. Credits were in the form of advance payments to help with insurance premiums and were based on income level.

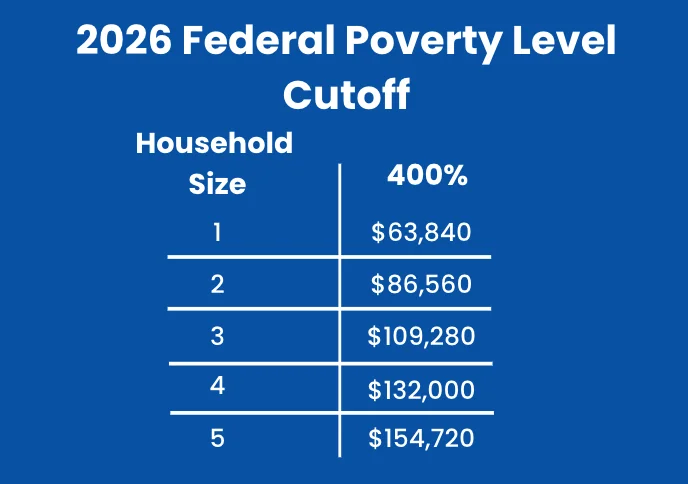

Initially, anyone whose income was below 400% of the federal poverty level was eligible to receive them.

But in 2021, things changed. That 400% cutoff was eliminated temporarily, and anyone could receive credits if the cost of their healthcare premium exceeded more than 8.5% of their household income. The amount of your credit would be reduced as your income increased, but you could usually count on receiving a credit of some amount.

If your eyes have glazed over thus far, here’s the newsworthy part:

As of the beginning of 2026, with the enhanced subsidies expired, Marketplace enrollees whose income exceeds 400% of the federal poverty level will again lose premium tax credits.

If that’s you—if your income exceeds the 400% amount by even $1—you’ll no longer receive any credit at all. If that happens, you could end up paying thousands of dollars more every year for health insurance depending on your location, income, age, and other factors.

How To Avoid “Falling Off The Cliff”

If you’re retired but haven’t yet reached age 65, you’re likely accessing health insurance through the ACA rather than Medicare. Depending on your income, you may qualify for a premium tax credit.

Keeping your income within the required range can help you stay within the ACA guardrails, something we actively monitor and guide our clients through as part of their broader financial plan.

At Curio, we’re using targeted tactics to help our clients stay safely under that threshold. Let’s walk through two key things you can do on your own:

1. Be strategic about income withdrawals.

When you’re drawing from multiple types of accounts, how you source your income matters just as much as the amount you take. Many clients have a mix of taxable accounts, pre-tax retirement accounts, and Roth accounts, each of which affects your taxable income differently.

By looking ahead and intentionally choosing which accounts to draw from over the next few years, it’s often possible to meet your cash flow needs while keeping reported income within the ACA guardrails. In some cases, that may mean temporarily using cash or Roth dollars, even if those funds are typically earmarked for long-term goals, to help minimize income and reduce overall healthcare costs during this window.

2. Time your capital gains

Another key part of that planning is monitoring realized capital gains. Investment sales, rebalancing, or unexpected distributions can all increase your taxable income, sometimes without it feeling obvious in the moment. We pay close attention to these moving pieces throughout the year so adjustments can be made thoughtfully and with the goal of staying within the ACA guardrails.

Need help navigating the ACA subsidy?

If you’re a retiree in your early 60s, the 2026 ACA cliff is real but it’s absolutely navigable with smart planning. It’s all about timing your withdrawals and capital gains to stay under that 400% FPL threshold.

If you need help mapping out those income buckets, reach out to us at Curio Wealth. We’re happy to advise you on how to pull income strategically and manage your capital gains. In the end, a little extra planning could save you thousands on healthcare costs while also setting up your retirement nest egg for the long haul.